Few foresaw problems pushing Columbia Gas System Inc. into bankruptcy court last year. But eight months later, there's some consensus on how – and when – the company is likely to work its way out.

Keep in mind that there are two bankruptcy cases here, separate but parallel: Columbia Gas, which employs 230 in Greenville, and its West Virginia pipeline subsidiary, Columbia Gas Transmission Corp.

The two have different creditors and circumstances. But they're expected to simultaneously present plans for working out from Chapter 11 protection – perhaps as early as this month.

Company officials and outside analysts agree: Any debt-reorganization plan filed in the weeks to come is merely a first step in a process that could take a year or more.

However, "Everything I hear is that Columbia is going to be able to work out of this," said Carl Ericson, an analyst for the American Gas Association. "They've taken a lot of prudent actions. This is not a prelude to something worse."

There's wide agreement, too, on the main problem to be ironed out in what's been called "a one-issue bankruptcy."

Columbia Gas blamed costly contracts with 4,700 natural-gas producers – signed years ago when market prices were twice today's – for forcing the bankruptcy.

The suppliers had tuned down Columbia's $600 million stock offer to buy out the problem contracts. But in August, U.S. Bankruptcy Court Judge Helen S. Balick in Wilmington let Columbia Transmission drop the high-priced contracts.

That's fine for the pipeline, which then cut its wholesale prices in a highly competitive market. But it left thousands of jilted suppliers with claims against the company.

Now, creditors "in the end might become Columbia shareholders," analyst Gerald Holtzmann said.

Sorting out those claims, putting a price tag on the suppliers' losses, paying out from the pipeline's assets – those are the tasks ahead in the Columbia Transmission case.

Attorneys in the Wilmington bankruptcy court call the pipeline subsidiary "Transmission" or simply "T-Co" – a shorthand distinction from the parent company Columbia Gas System.

The parent's debts look simpler. "Columbia Gas' reorganization is not the problem," said analyst Robert Lynch of Delaware Bay Co. The New York brokerage specializes in distressed and bankrupt companies.

Lenders cut off Columbia Gas' credit after the company suspended its quarterly dividend in June. Columbia Gas said it dropped its dividend because of Columbia Transmission's costly supply contracts, and a series of warm winters with low gas demand.

Columbia Gas' bankruptcy filing included $889 million due to banks and bondholders. The parent will pay its debts at 100 cents on the dollar – "That's been our statement from the start," spokesman H. William Chaddock said.

The July 31 filing caught Columbia Gas at a cash-poor point in its annual financing cycle. The company doesn't earn much in warmer months, but that's when the parent typically borrows money to invest in its subsidiaries.

But cash flow picked up by year's end, thanks to colder weather and Columbia Transmission's more attractive sales rates. And under Chapter 11, service on pre-bankruptcy debt was suspended – saving the parent company $31 million in the last quarter of 1991 alone.

"Columbia Gas creditors are going to get paid in full," Lynch said. He pointed to assets including solid subsidiaries in gas production and exploration. Added up, the assets outweigh Columbia Gas' debts.

Also among the parent's holdings: $1.35 billion owed to Columbia Gas by Columbia Transmission, secured by liens and mortgages. Much of that debt stems from 1985, when the parent loaned money to help the pipeline buy out high-priced supply contracts.

It's ironic, Chaddock said: "Part of the solution in 1985 became part of the problem in 1991."

Because Columbia Transmission's $1.35 billion debt to the parent is secured, it gets paid first under bankruptcy law. That puts Columbia Gas ahead of other Columbia Transmission creditors – including the gas suppliers whose contracts were dropped.

The parent is also owed an unsecured $360 million by the pipeline. For that amount, Columbia Gas is an equal footing with the jilted gas producers.

What's available to pay Columbia Transmission's unsecured debts? Lynch estimates the pipeline's value at $1.5 billion, plus $300 million in cash. Subtracting the secured debt owed the parent leaves about $450 million.

Both the pipeline and the parent have until March 30 to file debt reorganization plans in bankruptcy court; after that, creditors may propose other payoff plans for the debtors.

It's not unusual for courts to stretch such deadlines, though. But Columbia Gas and its pipeline subsidiary have made no decision on whether to ask for a second extension of the original November deadline, Chaddock said.

The plans are to spell out what the companies have to pay claims with. But the thorny issue remains: How much are the claims by Columbia Transmission's former suppliers worth?

Last year, Columbia Gas said the above-market-price contracts could cost the company $1 billion, and took a related $1.3 billion pre-tax write-off. Earlier, the company had offered $600 million to buy out the contracts – about 60 cents on the dollar.

It's now up to the gas producers to reckon how much their contracts were worth, and to put the estimates before the court by Wednesday. But that deadline is "really just the starting point for a lot of work" toward agreement on the contracts' cash values, one bankruptcy attorney said.

Columbia Transmission has been in talks with the gas producers to help evaluate claims, Chaddock said.

"To really estimate the damages to the producers, you have to estimate where gas prices are going to be" over the contract period, Lynch said. Also, some contracts included options that would vary the volume of gas sold to Columbia Transmission. "There are a lot of contracts, and they're all different," he said.

Once the value of the claims against the pipeline – and the value of the pipeline itself – are worked out, some kind of payoff plan can follow.

How long until Columbia is out of bankruptcy court? Last October, Chairman John H. Croom estimated 12 months to 24 months for the work-out. That timetable still holds, Chaddock said.

Analyst Lynch estimated the whole case could be wrapped up in a year.

On the other hand; it could take 12 months just to evaluate the producers' claims against the pipeline subsidiary, one Columbia Gas creditor said.

"No telling how long" Columbia Gas will stay under court protection, analyst Holtzmann said in January. Creditor lawsuits pending in state courts could extend the bankruptcy into next year, he said.

With a series of steps to boost sales, raise cash and cut spending, Columbia Gas System Inc. has propped itself up to compete in a tough market.

The Greenville energy company and its natural-gas pipeline arm sought bankruptcy protection last summer. The move will likely pay off, analysts say.

"Things look pretty good for Columbia going out a year from now," said Adam Sieminski, a Washington analyst.

But due in part to a long-term slide in market prices, "the environment Columbia is going to be coming back into is not going to be pretty," he said.

"Unless the economy really takes off, you're not going to see a tremendous increase in demand for natural gas. So these companies will continue to be under pressure," said Michael Clark of Del-Vest Inc., a Wilmington investment firm.

Let out of 4,700 above-market-priced supply contracts by a U.S. bankruptcy judge, pipeline subsidiary Columbia Gas Transmission Corp. nearly halved its natural-gas wholesale rate between August and February.

The new sales rate beats most of the pipeline's regional competitors, Columbia Gas spokesman H. William Chaddock said. But other sources of natural gas are still "far less expensive," said a spokesman for Delmarva Power & Light Co.

Still, lower sales rates combined with a colder winter pushed up income for Columbia's pipeline and retail businesses. Pipeline earnings jumped 23 percent to $49 million in fourth-quarter 1991.

"Columbia's business operations have been affected very little by the bankruptcy filings," said John H. Croom, chairman and chief executive officer. The parent company reported a 34 percent jump in quarterly net income, to $81.5 million.

The bankruptcies are "really more of a capital structure issue than an operational issue," said analyst Robert Lynch of New York brokers Delaware Bay Co. After working out of Chapter 11 in a year or so, Columbia "will pretty much be the same player they were before" – but with a new advantage from dropping the costly supply contracts, he said.

On the other hand the natural gas marketplace may be in for a shakeup. Federal moves to deregulate the pipeline industry may take effect in less than a year, analysts say – adding more pressure in an already competitive field.

In ability to compete under the proposed changes, "some pipelines are in good shape and some have a ways to go. Columbia is out there in the middle," Sieminski said.

Market pressures forced Columbia to trim spending several times in the last year or so. The company started 1991 with a $600 million capital budget. But in the wake of a warm winter, "we knocked $180 million out" of the spending plan, Chaddock said.

Of the cuts, $100 million would have gone to Columbia Transmission for projects such as new pipelines. Another $60 million would have paid to explore gas and oil sources.

Further cuts in exploration helped bring this year's capital spending plan down to $370 million.

The parent company also trimmed salaries in July – 5 percent for many employees, 10 percent for management. The cuts were partially restored in November. A hiring freeze went into place about a year ago; employees who leave are replaced as necessary, Chaddock said.

The company has also earned cash by selling off some businesses. January saw $95 million sale of Columbia's oil and gas subsidiary in western Canada. Last November, it agreed to a $128.5 million sale of its liquefied natural gas business, including a Cove Point, Md., terminal to a Shell Oil subsidiary.

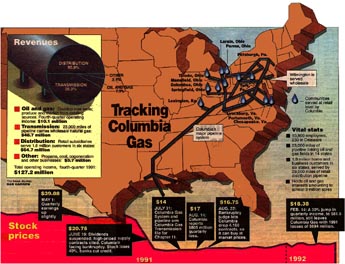

Columbia stock fell by 40 percent, of its value to $20.75 in one day last June, when the company suspended dividends and hinted at bankruptcy. Since

January, the stock has bumped along between $16.50 and $19. It closed Friday at $18.38.

Still, some investors look twice at the troubled company. Compared to other companies in bankruptcy, "We think it's a relatively low-risk investment that offers modest returns," analyst Lynch said. His firm specializes in troubled companies.

Said one broker: "People say, 'Should we buy Columbia now that it's

depressed?' But once they're out of bankruptcy, what's to keep then from doing it again?"

Such caution is "a common-sense point of view – but some people are always looking for a deal," he said.

Said analyst Holtzmann: "Columbia could prosper upon reorganization, but how well is a concern that gives this equity speculative appeal."